Insurers have been presented with a lot of regulatory guidance relating to vulnerable customers. Implementing it all will keep many insurance people busy. Yet all this activity needs to be seen within a wider ethical context. Grasp that context and your firm will achieve better and longer lasting results. Ignore it, or treat all this as just more rules, and your firm risks a big mis-selling fine.

Why mis-selling, you might ask. Isn’t this about service? Far from it. If a firm systemically fails to recognise, understand and respond to the circumstances and consequences of vulnerability, then this to the regulator is a form of mis-selling.

And for insurers, this situation is doubly serious if those circumstances of vulnerability are not also recognised in claims processes. Indeed, insurers need to look at all stages of their product lifecycle through a vulnerability lens. This means product design, underwriting, distribution, onboarding, renewal and claims.

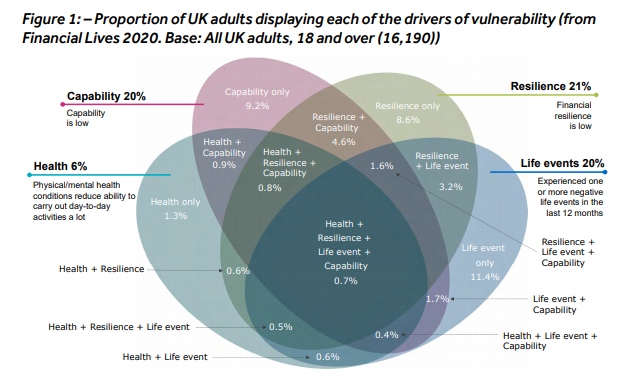

Let’s look at that wider ethical context first. Insurers have tended in the past to think of vulnerability in ways that assumed it to be a relative small and discrete group. For example, those with a disability, or very old. What the regulator’s Financial Lives survey shows is that at over 24 million UK adults, vulnerable people are far from being a small group. And the four drivers of vulnerability (health, life events, resilience and capability), and the way in which those drivers are often intertwined, shows that the group is far from discrete.

The New Vulnerability

So the mindset insurers need to adopt is less ‘them’ and more ‘us’. This was emphasised in a 2019 speech by Andrew Tyrie, then chief executive of the Competition and Markets Authority…

The rise of the digital economy has brought huge benefits to millions of people. But it has also rendered previously confident and capable consumers vulnerable to getting bad deals and poor service. This is not just people who are vulnerable on well-understood indicators: those who might be old, or on low incomes. It includes millions – perhaps even the majority – of the population, many of them ‘time poor’. They – us – are the “new vulnerable”. We are all vulnerable now.

Think about it. If live events such as bereavement, job loss and relationship breakdown are a driver of vulnerability, then every one of us will be vulnerable at some point in our lives. It’s what I’ve previously referred to as those micro-financial and micro-emotional crisis that happen, to us all. You need to built processes that reflect this. You need to build mindsets that understand that these processes will matter to you and your loved ones, not just some vague group out there in customer land.

This will of course be a big undertaking. Yet when you look at the regulator’s vulnerability graphic below, the first thing that you notice are a lot of low percentages. Is this vulnerability guidance a sledgehammer to crack a nut? Far from it. One percent of 2.4 million people is 24,000 people. As for the 20% of UK adults who experience one or more negative life events over a twelve month period, that’s 480,000. These are lots of people, lots of your customers, lots of people like you.

Raising Up Assumptions

This mindset change, of seeing vulnerability as about ‘us’ and not ‘them’, needs to happen across your firm. This adds up to seeing vulnerability not as a stand alone theme, but as integral to your firm’s culture. This can actually be an empowering process. In making it part of your culture, you’ll come across instances when unwritten assumptions can be surfaced and examined.

I recall a time early on in my role as Head of Risk and Insurance at what is now Motability Operations, where virtually every customer was vulnerable. The insurer was working under a service contract that they felt could be improved. To their credit, they undertook their own customer research into what services were valued most. The key metric under the existing contact came in at No.22, while No.1 and 2 had never been measured by any motor insurer.

Yet when we thought about it, those first and second most valued metrics made perfect sense. The people who wrote the contract (not me!) had chosen what they thought was important, assuming that customers would think likewise. And to the insurer’s further credit, their response was not to question the need for those two metrics, but to address how to be the first motor insurer to measure them.

So these assumptions need to be opened up and examined, about what people in different vulnerable circumstances actually want. Is your firm asking those questions, or is it just jumping to assumptions? How is this then reflected in the data you collect, in the data visualisation you use for reporting? And how is this then reflected in targets setting and performance evaluation?

The Most Challenging Assumptions

Some of those assumptions will be buried deep inside the decision systems that your firm has built as part of its embrace of digital. This can be where some of the most challenging assumptions will be found. Does your underwriting use credit scores for pricing? If so, how do you then justify that when considering your approach to people with low financial resilience? With difficulty, I would say. And how do your claims people justify using credit scores in settlement decisions? Pretty impossibly, I would say.

Yet we know that these things are happening in the market. Some of them have become normalised, seen now as just part of how the market works. So a commitment to meeting the needs of vulnerable consumers will involve facing up to some challenging ethical dilemmas. How good are your people at handling such dilemmas?

What Type of Firm are You?

Another consequence of that move from seeing vulnerable consumers as ‘us’, not ‘them’, is around the type of relationship you want to have with your customers. If your firm sees itself as being digitally led, then this would point to vulnerability being more of a challenge for your firm. However, if your firm sees itself as being customer led, then vulnerability is going to be a much smoother journey.

We know of course that firms often talk of being both digital and customer led, seeing them as two sides of the same coin. One way of questioning this is to look at their executive team. Are there two CEOs? Probably not. So in reality, they’re either digital or customer led. Most often such firms focus on the digital, assuming that this will just naturally be good for customers. It’s a bad assumption to make about digital, let alone your customers.

As I outlined in this earlier blog post, customer centric firms focus on relationships, aligning their underwriting and claims systems (digital or otherwise) around them. The regulator’s guidelines on vulnerability will therefore be an asset for such firms, showing them ways to further develop those relationships, often when most needed. You can see in the regulator’s Financial Lives report how this can go a long way towards building relationships of trust.

Why are these People Vulnerable?

Some firms, confident in their purpose and culture, will go a step further. They will look at the data flowing from the regulator on vulnerability and explore it further. The question they will ask is this: why are these people vulnerable? Let’s explore this through an example.

Why do some people have low financial capability? And from this, how might my products and services be exacerbating this, and what can I do to change this. One obvious avenue is policy wordings, with some as long as a Tolstoy novel and requiring a university education to understand. I know of good work being done around this by some firms.

My point is that insurers committing to treat vulnerable consumers fairly need to see themselves as in some way part of the complex system that brings about that vulnerability. Now, some of you may have difficulty with that, but I urge you to stand back from your immediate reaction and think about it a bit. Some vulnerabilities don’t just evolve out of nothing.

They arise from circumstances that may be financial, such as those case studies in the Financial Lives survey where a turned down claim started someone on a downward spiral. Now, I’m not saying ‘just pay all claims’. What I am saying is ‘be sure your claims decisions are thoroughly fair and give appropriate recognition to vulnerability’.

Another circumstance from which vulnerability can arise is in relation to family obligations, such as looking after children or elderly relatives. How flexible are your people policies? Or those of your volume suppliers? Of course all these people are employed, but remember that not all vulnerable people are unemployed. It’s more nuanced than that.

Summing up

Insurance is part of so many aspects of its customers’ lives. This means that with nearly half of all UK adults being vulnerable at some point in their lives, every firm needs to take vulnerability seriously. In terms of how they should do this, here’s a recap of the thoughts I’ve raised above:

- Vulnerability is not an extra cog to be added into a corporate system – it has to be a feature of how that corporate system is designed and used, part of ‘how we do things round here’.

- Thinking seriously about vulnerability will raise up some hidden assumptions about your customers and these will need to be examined carefully. This won’t always be easy, so get help.

- The way in which you approach vulnerability will speak volumes about whether you are a digitally led firm or a customer centric firm.

- Part of your approach to vulnerability involves examining the decisions being taken by your underwriting, claims and counter fraud systems. How impact might they have vulnerability? Expect vulnerability to feature in the regulator’s forthcoming data ethics review.

- And finally, how might your firm be adding to some aspects of vulnerability? Insurance is so integrated into everyday life that this question cannot be avoided, despite being a difficult one to face up to.

Let’s end with a quick look back in history. In Victorian times, there were huge numbers of vulnerable people in this country. And to meet the needs of many of them, a new branch of insurance evolved: industrial life. And the successful industrial life firms were not just successful, but enormously and disruptively successful. My point is that our future can achieve the same as it has achieved in the past.